|

Getting your Trinity Audio player ready... |

Unproductive strategy meetings and corporate political drama wear heavy on the soul, and I often found myself drained early in my career when I felt that I was spending 80 percent of my time planning and 20 percent of my time doing actual work. This is because I don’t care to waste my time on things that don’t matter.

Throughout my career, there have been many moments where things, committees, or childish corporate drama have interfered with my goals and the goals of the institutions for which I’ve worked. When things like this begin to occur too frequently, I generally change roles because I don’t particularly care to work with children, as that was not my professional aspiration.

So, I care about execution a lot: my execution, my team’s execution, and the execution of the company for which I work. But not everyone does, and my conjecture is that over time companies that forget to focus on what matters (i.e., a pretty good strategy and relentless execution) will fold to a competitor who is nimbler and more focused on eating the complacent’s lunch.

Your Margin Is Someone Else’s Opportunity

Start-ups live and die by execution. If you can’t execute to deliver a differentiated product or acquire new customers—and do so quickly—your business will fail. I saw it happen firsthand at Fast.

This hyperfocus on execution is a direct consequence of venture capital because, for the most part, start-ups are quite literally running out of money (i.e., time) the entire time they’re operating, which is a great incentive for getting something done.

Established incumbents, on the other hand, don’t have the same incentive to execute. Instead, large corporations tend to focus on the following:

- Protecting existing revenue

- Minimizing short-term risk

- Strategizing against competitors

- Dealing with internal corporate bickering

When a company is large enough and has sufficient scale, these priorities seem quite reasonable. But the executives focusing on them have forgotten that the world is changing—quickly. Software and innovation compound in a way that lets businesses—particularly technology companies—leave their competition in the dust. So, while risk-aversion may be an acceptable strategy in the short term, it’s certainly not a good business strategy in the long term.

This behavior is not true of all big companies, and I believe there is a new era of management focused on disrupting the legacy model of death-by-endless-PowerPoint-meetings.

In fact, we are living through the transformation of one company at this moment as Elon Musk, one of the greatest capitalists of all time, takes over Twitter and explicitly addresses meetings and work output.

But this all leads me to a natural question: why exactly do big businesses place so much emphasis on strategy and meetings?

Alignment Feels Good

When you have a large organization, you typically have to spend a lot of time checking off boxes, building consensus, strategizing, attending meetings, and managing stakeholders.

These are all reasonable things within the context of a large company that’s trying to achieve alignment across several different teams and departments, and it certainly feels good to show off a fancy PowerPoint during a meeting or cultivate a sense of “togetherness.”

But what feels good and what is actually good are rarely the same thing (in fact, I’d generally argue the opposite).

This becomes clear when you consider that planning- and alignment-related tasks are never free. They cost the business time, energy, and often employee satisfaction. Moreover, these tasks are often completely unrelated to the core skill sets of the people doing the work, and they also may not even be correlated to the success of the work in question.

That’s not to say planning, alignment, and strategizing are bad—that would be stupid. But there is an optimal balance between planning and execution that most teams haven’t yet reached.

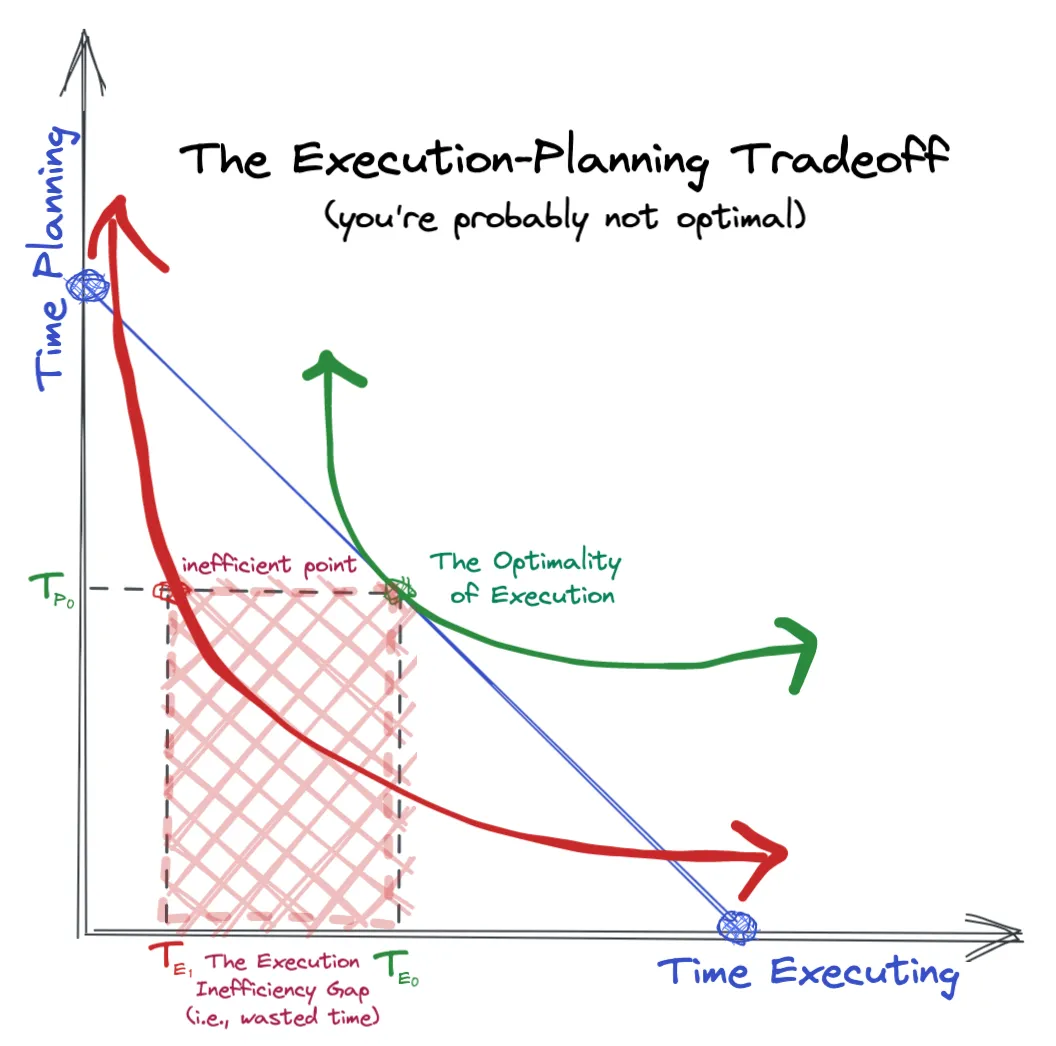

The Execution-Planning Tradeoff

Note: This is a modification of Indifference Curves and is designed to reflect how cofounders, start-ups, and especially big companies waste time. You’re probably operating at the inefficient point Te1.

This diagram says a lot but in short, you—like most executives—are probably over-planning.

Start reflecting on your day-to-day: how much of your day do you spend on doing (building a product, feature, ad creative, etc.)? Are all of your meetings actually constructive and helpful for executing on the output you’re trying to produce? Or are most of those meetings just time wasted on making people feel good?

How much of your day do you spend on hard work?

The kind of work that is frustrating, mentally taxing, and stressful but that also proves that what you are doing is worthwhile and not trivial? The kind of work that reinforces that what you’re doing will make a real impact on someone or something?

Find that work, grapple with it, overcome it, and relish in it. It’s what makes your work meaningful—and it will make you an execution master.

Francisco Javier Arceo has spent a decade working in fintech at AIG, the Commonwealth Bank of Australia, Goldman Sachs, Fast, and Affirm in roles spanning software, data engineering, credit, fraud, data science, and machine learning. He holds graduate degrees in economics and statistics as well as data science and machine learning from Columbia University and Clemson University. He is an angel investor and limited partner in the Fintech Fund.